The third powerful motivator was a competitive nature. In fact all the brokers I knew seemed to posess similar characteristics. Our employers understood our motivations very well and were quite intentional about the kind of people they hired. They were expert at using these motivators to great advantage, both for themselves and for us.

The numbers game of sending out so many mailers, followed by so many telephone calls, followed by so many in-person meetings led to so many new clients. It became monotonous at times, but I remained motivated out of need, idealism, and competition. The last, competition was almost constantly fed, by an uninterrupted stream of sales contests.

There were contests for selling limited partnerships of oil & gas, real estate development and apartments and investment tax credits. There were even low income apartment deals designed specifically to lose money for our wealthy clients’ tax write-offs. The top tax bracket was 70% then. There were mutual fund wholesalers in our offices constantly and each one had an incredible promotional incentive trip to some exotic locale. One had to wonder how the company could afford such extravagance and still make any money for the target of their funds (were we the target or were our clients the target?).

After a brief stint with the partnerships and funds, I gravitated toward individual securities (particularly stocks) and managed money (particularly growth). I moved most of my clients into my firm’s portfolio management platform which worked pretty well for a while, but I quickly found myself apologizing or explaining moves that I would not have made myself. I became convinced I could do a better job for my clients. What’s more there would be no one with which to share the credit or the blame. That thought had a strong appeal to my competitive nature.

Inspired by great managers of the time like Warren Buffett, Peter Lynch, and John Neff, I read extensively and trained myself and then received formal training at my subsequent firm, Wheat First Securities. My foray into full-time discretionary management coincided with the early days of the Information Age. As an early technology adopter of PCs and the requisite software to make my job easier, I was strongly convinced of the powerful wave that was to sweep our economy, well in advance of the average investor, or money manager for that matter. I had an advantage that Peter Lynch called buying what you understand. Peter believed that individual investors had inherent advantages over large institutions because the large firms would not or could not invest in smaller companies because the value of the company was too small to make a meaningful impact on their assets, or because they were not yet on analysts’ and fund buyers’ radar. As an early adopter of technology, it became my investing expertise.

As the Information Age rolled along, I became fascinated with the growing wave of “disruptive destruction” where older technologies were being replaced by new ones. It seemed the cycles of destruction were becoming shorter and shorter at an exponential rate. Even the traditional rules of investing were being thrown out by many experts. The old value metrics seemed ill-suited to meet the light-speed requirements of the new “Information Age.”

As our returns and success compounded during the 90’s, our clients began to adjust their lifestyles in remarkable ways and we could not have been happier for them (or ourselves). Common were phone calls from ecstatic clients thanking us that they could put in a pool, re-decorate the house, buy a sailboat, or a Porsche - for cash!, or take that pan-European trip with the whole extended family. Some even took extended sabbaticals to spend their new-found treasure. Prospective clients were waiting in line to sign with us, enthusiastically recommended by our clients for our money-making abilities.

Our aggressive growth model attracted the most attention. From March 1990 through March 2000 the model generated a compound return of 26% per year for clients. Over those 52 quarters returns were as high as 59% in a quarter! For thirty five quarters or two thirds of the time, clients received positive return reports from us. And more than half of them were above the 30-year averages for stocks at the time which was 12%.

Of course there were some big losers too. The worst quarter saw a decline of 57% and seven quarters saw losses of greater than 10% (40% annualized). It was interesting how huge gains made people more accepting of huge losses, but the real tests would come.

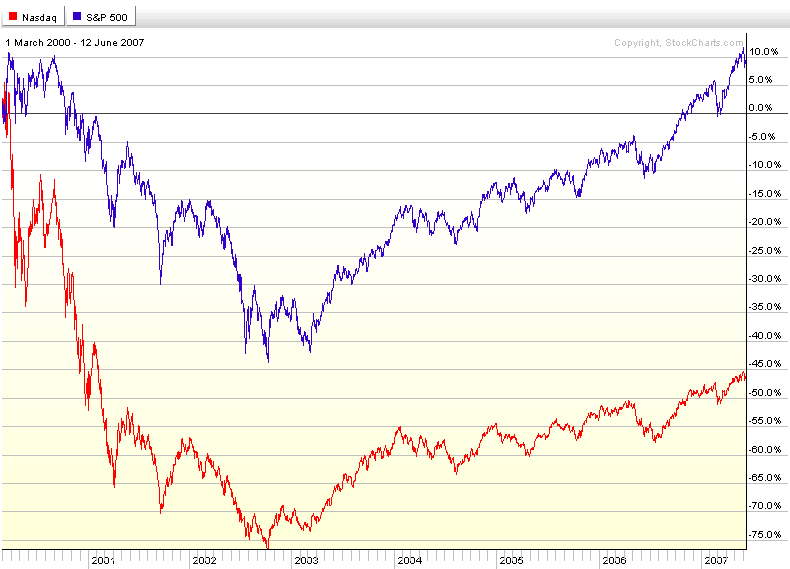

In March of 2000 the Internet Bubble exploded sending stocks tumbling. The NASDAQ, home of most technology stocks at the time fell 50% by the end of 2000. It would fall another 25% for a total of 76% to its bottom reached October of 2002. The S&P fell 43% before it bottomed the same time. Of course, in addition to the Internet crash, there were other ‘disruptions’ such as 911, war with Iraq, accounting scandals and Enron.

Needless to say, these events coupled with huge mounting losses took their toll on our client base. The new clients, the ones we refer to in the industry as “hot money clients” (those who chase top returns) were the first to leave. Then some of our older clients began to leave convinced we would not recover their losses. While we added significant diversification, moving away from technology, our portfolios continued to decline with the markets. Growth stocks were dead and value stocks were in.

During this time Alan Greenspan, Chairman of the Federal Reserve took interest rates to record lows and began pumping money into the economy to replace the billions that had evaporated in the stock market. The next wave of funds leaving came when low rates began a bull market in real estate – and the next bubble began to inflate. My argument that stocks were cheap and would come back with far better returns than real estate carried little weight.

While my clients had done better than the benchmarks we used to measure their performance and they had more money than they would have had if they invested themselves, they were still leaving, unhappy. Even though I had accomplished my objectives of beating my benchmarks, I had somehow fallen short of meeting the expectations of my clients.

Soon after reaching this stark realization, I had a Damascus road experience. It came through three close friends. The first was a client who left saying she was unhappy, not so much with her performance, but that we never talked about what she wanted to do with her money.

The second (same day) came when a good friend, with whom I had started my career, showed me some software he was using. I was fascinated, particularly because it put the client squarely in the center of the process.

Later that same day I received a phone call from Dave Loeper, an old friend and mentor from my Wheat First days and founder of a company I had invested in when he and I had left Wheat six years earlier. His company was known as Financeware. Dave, was calling regarding a deadline to get signatures from his angel investors.

Dave would spend the next hour and a half (time he really didn’t have) converting me from a performance manager to a wealth manager. He asked me a couple of questions that still resonate with me today. “Sam, what value do you bring to your clients?” My answer continued to belie acceptance of his assertions when I said, “I deliver portfolio returns to my clients that are superior to those they can get on their own or with indexes.” He then asked “can you guarantee that?” When I responded that obviously I could not, he asked one more time: “What value do you provide to your clients?”

In that moment it became clear that my clients deserved better than a performance-driven value proposition that is truly no more than a hope for success. I spent the next several months learning as much as I could about Financeware’s program known as Wealthcare. We converted our entire business model from a portfolio focus to a client focus. Conversations with clients became incredibly authentic. It is not an exaggeration to say that I learned more about my clients in the first hour of an initial Wealthcare plan meeting than I had learned in the 5, 10, or 15 years of managing their assets.

Validation that we had made the right choice came quickly. Client plans revealed significant opportunities that had been ignored by our portfolio/return-centric approach. We realized dramatic improvement in the goals our clients valued without sacrificing their current lifestyles. It became clear that the very methods I was using before to create opportunity for my clients was in fact creating uncertainty that hid or diminished them. For instance, in almost every case, we found that our clients were taking more risk than was required to meet or exceed their goals. As a result, our overall portfolio risk as a firm dropped substantially.

As you look at the graph above you can see there was a second drop of greater proportion in the S&P 500 index (in blue) and a much lower one in the NASDAQ (in red) in 2008 and 2009. Most of the nation’s banks and financial companies reside in the S&P 500. As they were hit the worst, the NASDAQ did comparatively better this time around.

So how did we do? We are focused on confidently meeting clients’ goals with sufficient wealth, not return, so graphics don’t tell the full story. Perhaps the greatest difference between 2000 and 2008 came in our telephone traffic. It pains me to think back to 2000 and the many panicked calls I fielded with little more than “stay the course, it will come back” for comfort.

In 2008/2009 our phones didn’t ring with the frenzied calls of 2000. Conversations were mostly prompted by us as we doubled and tripled our efforts to stay in touch through challenging times. When our clients asked how ‘we’ were doing, we offered them substantive information from their latest stress tests which showed they could be confident of meeting or exceeding their goals, despite market declines. It helped significantly that most had experienced significantly less volatility than the 37% declines of the S&P 500. In fact most (86%), required no changes to their plans as a result of the declines.

Today, with six years of Wealthcare experience for more than 75 families, I can happily say that our clients are empowered to live more abundant and purposeful lives as a result of our dramatic change in course. We and our clients no longer take life as it comes, we design lives with purpose.

No comments:

Post a Comment